# 5. Money flows, inflation and unemployment.

At first glance, the mechanics of how money flows through an economy, is a technicality, a detail for economic geeks to worry about. Textbooks will often give only the most crude analysis, missing the details required to make any useful deductions. In this chapter we will go a few steps deeper and demonstrate that important economic phenomena like unemployment can be understood in terms of money flows. We will start with a simple model, then add in some essential extra details like the money creation and destruction we learned in chapter 1.

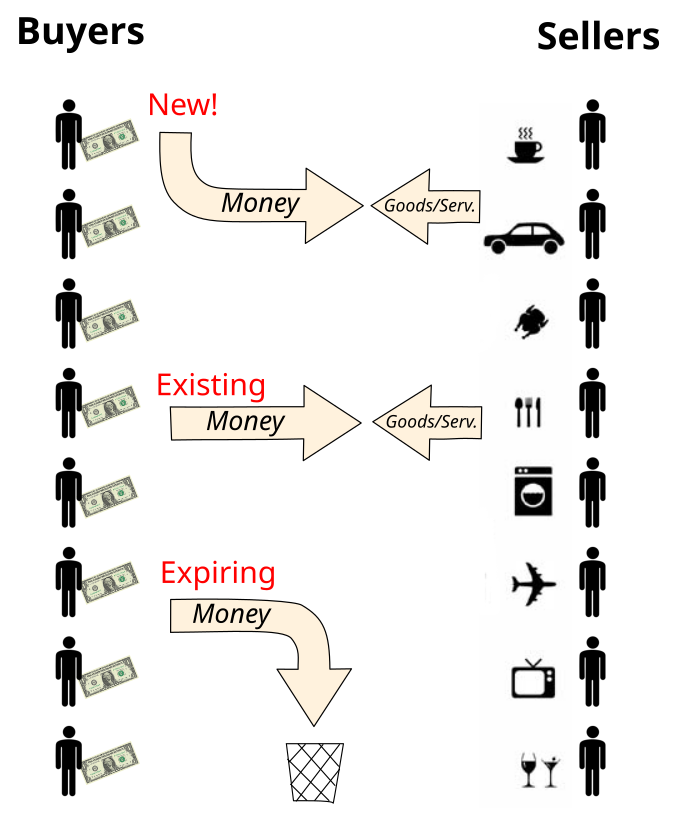

The first simple model can be understood by considering the diagram below:

A simple model of money flowing in an economy

In the economy, people are continuously using money to purchase goods (and services). For the sake of the analysis to come, we need to imagine that during any short time interval T, all the people that are making purchases in this period are metaphorically lined up along the left hand side of our diagram, whilst all those making a sale are lined up on the right. It should be noted that in any individual time period there is additional money (not shown in the figure) that is not spent on anything, it is stationary. Similarly, there are additional items (also not shown) that are for sale, but that were not purchased.

The interval T, could for example be a second, a minute or an hour, but importantly, not zero (you can't get anything done in zero time). Breaking down continuous processes into a succession of discrete steps is standard practice for engineers modelling real world phenomena and is used in everything from aerodynamics to atomic physics. In the language of computer simulations, each time step is known as an "iteration".

Armed with this model, it appears that the rate of flow of money from left to right must be exactly equal to the rate of flow of the value of (i.e. price paid for) goods traversing from right to left. This fact has led some economists to conclude that the amount of money people receive on aggregate selling their goods, is exactly the right amount to be able to purchase the same amount of goods at the next iteration. This idea is known as Say's law after the economist [Jean-Baptiste Say (1767–1832)](https://en.wikipedia.org/wiki/Jean-Baptiste_Say). When we add more details to the model later on, we will see that Say's law, whilst approximately correct, is generally not exactly so, and the slight discrepancies have important effects.

### Shifting sizes of sectors - money as a signal.

The people on the left hand side of diagram are of course free to choose what to spend their money on. The proportion of the total flow that is spent on each type of good or service may fluctuate over time. This could happen for many reasons, including changes in taste or advances in technology. So for example spending on old style film based cameras started to fall around the year 2000 while at the same time there was a corresponding rise in spending on digital cameras. Changes in what people spend their money on will have impacts upon employment patterns in one of two ways. It depends upon whether the manufacturers of the going-out-of-fashion choice are also well placed to manufacture the newly-fashionable choice. For example, if a shirt manufacturer finds that its sales of green shirts are falling whilst demand for blue shirts is rising then it can simply switch production from one colour to another. But if the new choice involves a radical change in technology, it may be that the company making the going-out-of-fashion items goes out of business entirely, whilst another pre-existing or start-up company expands, taking on new workers. Either way, there is not necessarily any long term reduction in the number of people employed, simply a change in who makes what. Looking at an economy this way reveals how the rate of flow of money into the various sectors can act as a signal, guiding workers away from the production of things that people don't want any more, towards the production of things that people do want. The choice of things that people demand and the way that these choices change over time are highly complex, and yet under a free market the adjustment of production to match people's desires happens automatically. No central controller is making any decisions about what should be manufactured. It is a self-regulating system. This is just one of the observations that leads free market economists to insist that governments should leave an economy to its own devices.

It should now be obvious that there is a relationship between the rate of money flow into a particular sector and the likelihood of that sector gaining or shedding jobs. Roughly speaking, if the total flow of money to one sector decreases you may expect it to shed jobs, whilst if the flow rate to another increases you could expect it to gain jobs. But the precise nature of this correspondence is not so straightforward. For example, if there was a gradual increase in the amount of money in the economy, say 10% extra per year, but the *proportion* of the money that flowed into each sector remained constant, then the amount of money flowing to an individual sector would be increasing *without* causing an increase in the number of people working in it. Perhaps it would be more accurate to say that it is the *proportion* of the total flow, rather than the absolute amount that determines whether a sector will gain or shed jobs. Whilst this may be a plausible end result, it seems unlikely that individual small business owners are making decisions about whether to expand or contract on this basis. Small business owners do not generally make estimates of the rate of flow of money in the economy as a whole. It is much more likely that they will be expanding or contracting according to other factors that they are observing directly themselves, as shown in the following table:

**Likely changes in employment in a sector based on factors readily observable by business owners.**

| **Factors that may lead to more workers in this sector.** | **Factors that may lead to fewer workers in this sector.** |

| ----------------------------------------------------------- | ------------------------------------------------------------- |

| Profitability is high and or rising. | Profitability is low and or falling.. |

| Order books are full and/or stock of unsold produce is low. | Order books are empty and/or stock of unsold produce is high. |

There are two separate mechanisms that will drive a sector to expand in response to more money flowing into it. Mechanism one is simply that the businesses maintain their current prices and take on more workers in order to increase their rate of production so as to meet demand. Mechanism two is that they increase their prices so that the amount of orders slows down to a rate they can cope with using their current complement of workers. This will result in increased profits, but then upon observing these unusually high profits, entrepreneurs and workers from other sectors will become tempted to migrate into this high profit sector. Undoubtedly both mechanisms will be at play to some degree. A corresponding set of arguments can be made in the case of low profitability / empty order books leading to lower employment in a sector.

So now we are beginning to see some basic features of the model, but in order to understand some trickier phenomena, we must add money creation and destruction. We learned in chapter 1 that money is created out of nothing when loans are made and it is destroyed as loans are paid back. This means that our money flow diagram must now be modified as follows:

A more complete model of money flows

In the initial diagram, all money that was used for spending, consisted of pre-existing money that was earned in some earlier iteration by someone who, at that time, was on the seller side of the diagram. Taking into account the workings of our monetary system, we can say that some small fraction of the money being spent will have come into existence afresh on this iteration. Also some fraction of the money earned in previous iterations will be expiring out of existence in this iteration because it is being used to pay back the principal on a pre existing bank loan. The amount of money being created and destroyed per iteration do not necessarily balance. Most of the time the economy will be in one of two phases:

* a growing money supply environment: on each iteration there is a net injection of new money not obtained during any previous iteration

* a shrinking money supply environment: on each iteration there is a net loss of money

We can now see that Say's law is in trouble. The amount of money earned on one iteration may not be enough (or may be in excess of enough) to purchase the same amount of goods at the next iteration depending on the amount of net money creation/destruction. There is however a possible saviour. We must not forget that the advertised prices of the goods can also change from one iteration to the next. If, in a given iteration, there was a net change in the money supply of X%, maybe the prices could have changed correspondingly. Whilst this may indeed be possible, in practice the probability of it matching precisely is incredibly small.

So Say’s law is not *strictly* true, but it is *approximately* true or to be more precise, there is a tendency towards it being true in the long run. Maybe it should have been called 'Say’s tendency'. Any period in which there was insufficient money to buy as many goods as were purchased on the previous iteration, would tend to increase the stock levels of producers, which would act as a signal or inducement for sellers to lower their prices. Conversely any period in which there was an excess of money required for purchasing as many goods as were purchased on the previous iteration, would tend to decrease the stock levels of producers, which would act as a signal for sellers to raise their prices.

The description just given would seem to indicate that the system should run smoothly with prices being exquisitely adjusted up and down just enough so that in the medium term everything on sale will get sold. This process is not quite as automatic and responsive as it sounds. The problem is that in reality, manufacturers in many sectors are very reluctant to change their prices frequently. This reluctance is for a variety of reasons:

* Fear it will alienate customers.

* Accounting complexity.

* Cost/complexity of changing any marketing material that mentions the price.

Surveys have shown that on average, companies change their prices around two times per year. This reluctance to change prices rapidly in response to changes in stock/demand is known as “friction” or “sticky prices”. It means that should there be a reduction in the rate of money flowing into a sector, the corresponding drop in prices can be slow.

To make this lack of responsiveness even worse, when a product is not selling quite as well as hoped or planned for, a manufacturer will have many possible explanations that are not connected to changes in overall money flows. Maybe their latest marketing strategy was wrong, the weather, something in the news/media, variations in the performance of their competitors, staff performance failures. Businesses are not on a hair trigger, ready to adjust prices at the slightest signal, far from it.

### Consequences of a surprise fall in the money supply

Imagine for a moment that something causes a surprise fall in the money supply, so the rate of flow of money into all sectors reduces. A naive view might be: “OK, so there’s a lack of demand, never mind we’ll just lower our prices, take a bit less (nominal) profit, but that doesn’t matter because *everyone* will be lowering their prices everywhere, so our numerically smaller profits will buy just as many goods as before. So everyone’s happy, nobody loses their jobs and we can all carry on as if nothing had happened”… but this view ignores several important real world issues:

1. The time between purchasing raw materials and receiving money for the end product.

2. Money that may have been lent to businesses, at interest, in order to make their products.

3. Long term agreements that are costs, e.g. rent or inflexible supply contracts.

All three factors correspond to a long gap between a company paying out (or agreeing a price to pay) for the costs of production, and the receiving of money through sales. The fall in the money supply now means that the agreement of costs was slightly wrong. Too much money has been handed over or promised to suppliers given the, now reduced, level of income. This will cause the profitability of a company to fall or even become negative. In the maelstrom of economic activity, this effect may not be obvious when looking at the state of an individual business. After all, the fortunes of a company may fluctuate up and down for many reasons unconnected with any subtle fall in the money supply. But in any complex economy with millions of businesses, there will always be some that are teetering on the edge of failure and the additional stress of a falling money supply can be the thing that pushes them over that edge. Note that a company that is teetering on the edge should not be considered as a company that was going to fail anyway. There are countless successful businesses that have gone through at least one period in their history, where they have been close to failure but pulled through.

In conclusion a surprise fall in the money supply is harmful to an economy and will have a tendency to increase unemployment from companies going bust.

### Now we have a paradox to solve

We now know that Say's law does not strictly apply from one iteration to the next. But then this introduces a potential mystery: If Say's law is false, and we have a falling money supply (which can occasionally last for years) and we were in a semi-continuous state of not having enough money to buy all the goods that are for sale, then wouldn't there be an ever-growing pile of unsold goods? Where is that pile?

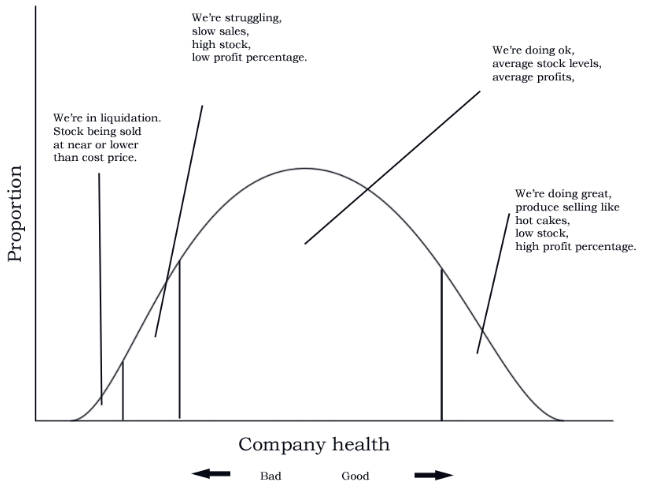

In order to answer that question consider the following: Under almost any economic conditions, the health of individual companies is bound to correspond to some sort of range in profitability due to natural variations. Something along the lines of the diagram below:

From this diagram we can see that there is always some component of the goods being sold that is on sale at 'distressed' or 'fire sale' prices. These goods were made by companies that are in the process of laying off workers or going bust. This will tend to be goods that remained unsold for too long at its previous price initially planned for by the manufacturer.

If the money available for purchasing is shrinking, then this will have a tendency to increase the average time it takes for goods to be sold. This in turn tends to increase the likelihood that companies will fail and so increases the proportion of goods that will, at a later iteration, be on sale at distressed prices. So a period in which the money supply shrinks, tends to set in train a sequence of events that results in lower prices which enables all the goods to be purchased. But you will notice that just because all the goods get purchased does not mean that all the sellers are making a profit and keeping their jobs. Purchasing goods at distressed prices will not necessarily rescue the manufacturers of those goods from shedding jobs or shutting down. It may well be that the distressed price is below what the goods cost to manufacture and so it is simply not possible for the manufacturer to stay in business even if its workers agree to a pay cut.

### An expected fall in the money supply, i.e. continuous falling over sustained period

Some people reading this may say, OK, so a *surprise* fall in the money supply may cause some businesses to fail, but surely *expected* deflation must be harmless because business owners will see it coming and will correctly prepare for it in advance. Whilst this may sound theoretically plausible, in reality it is unlikely for three reasons which we shall consider in turn.

1\. Sustained and steady deflation is a relatively rare state in an economy. Deflation is often associated with crises and both governments and central banks tend to fight against it. The news media is unlikely to give the message "after the recent period of deflation, we expect more of the same for years to come, so you'd better all adapt to it". Instead it is more likely to be "The central bank is determined to bring the economy back to positive inflation and is doing everything in its power to achieve this". Another thing to consider is, how long a period of deflation is required before people begin to assume it’s going to continue. If inflation has been positive for decades, will six months of deflation convince people that deflation is going to continue for a substantial period into the future? Will a year convince people? Maybe two years? The answer is not obvious.

2\. Do business owners even consider future inflation/deflation at all? With some notable exceptions, inflation has historically been a small percentage change each year. If a business owner is planning a new product launch in six months time in an environment where inflation is less than, say 3% per year (either positive or negative) then the potential (approximately) 1.5% difference that inflation/deflation makes to the optimal final selling price will often be ignored altogether.

3\. As discussed earlier, the proportion of money flowing into each of the possible sectors of the economy is not set in stone. There will be natural variations. So a period in which the money supply is shrinking overall, will not necessarily mean that all sectors will experience the same reduction in flow rate. This leaves scope for individual sectors to be taken by surprise by a fall.

### Very low inflation is problematic

Some people may say, "OK, so deflation is bad but very low positive *inflation* must surely be harmless, or even a good thing"... well actually, not. The published inflation figures correspond to the average inflation of all sectors, with some sectors having a rate higher and others lower. This means that the lower the rate of (positive) overall inflation, the greater the probability that some sectors are undergoing harmful deflation. Around the world it appears that an inflation target of 2% has become popular, but there is little or no research that actually supports the selection of this particular rate. It may well be that 3, 4 or 5% would make an economy work better.

### More arguments for not-too-low inflation

Another argument for having positive and not-too-low inflation can be derived from the concept of "veil of barter". This odd sounding expression needs a little explaining with a thought experiment:

Imagine a primitive society without money. All exchanges of goods would have to be performed using barter, i.e. direct exchanges of one good or service for another. This would of course be very inefficient, largely because of the problem of the so called 'double coincidence of wants'. For example, a fisherman who desired a new pair of shoes would need to seek out a shoemaker who desired some fish - a tall order. But now let us introduce a wizard with mind reading powers (this is a thought experiment after all), the wizard knows both what everyone in the society wants and what everyone has to offer. Once a day everyone gathers in the marketplace and the wizard announces the optimal set of barter transactions that satisfies peoples desires as much as possible and the exchanges then take place according to the wizard's prescription. The fisherman would get his shoes, even if there was no shoemaker that desired fish, so long as some people desired fish and some people made shoes, there would almost certainly be some, perhaps complex, set of transactions that was agreeable to all parties and that resulted in the fisherman getting some shoes. The addition of the wizard transforms the inherently inefficient barter economy into an efficient one. Obviously this scenario is not possible in the real world but it is said that if money was introduced to a primitive society then the new flexibility in trades acts in much the same way as the wizard. Money makes an efficient set of exchanges possible. This is the idea of a 'veil of barter' - it is the notion that money can act in a way, such that that the exchanges made are no different to that which would take place in an efficient barter system. It is for this reason that many models and computer simulations of economic systems often ignore money altogether. The models simply look at the produce and desires of the population and then assume that the goods get exchanged optimally. This is not just true of simple models used by students, but even ones used by governments and central banks.

A critical issue to notice about the "barter+wizard" world is that at any one instant the people in the society can only be in possession of real goods. There is nothing which acts as a token which can be redeemed for goods at a later time. A characteristic of real goods is that in general they decay over time. They rot, rust, become redundant etc as discussed in chapter 3. Now if money had the characteristic that its rate of change of value (due to inflation or deflation) was different to that of the typical rate of decay of real goods, then we would expect that the transactions that occurred in a world with money would be *different* to that which we would see in a barter world. The 'veil of barter' would break or at least become less true.

So if we assume that the barter+wizard system is optimal (even if only theoretically), and if we want money to simply enable the same transactions that would occur in such a world, then this is best achieved if money "decayed" in the same way as real goods. It seems likely then that the optimal rate of inflation should probably be more than 2%, after all there are not many real world goods that decay as slowly as that. Perhaps a more realistic rate might be of the order of 5%, perhaps more.

### Money in economic models

Hopefully from reading this chapter you can get some idea of the impact money creation and destruction by banks, has on the behaviour of an economy. One might therefore assume that the economic models used by professional economists will certainly include the role of banks and money. But quite staggeringly, they rarely do, at least not mainstream economists. Just as one example, a leading textbook used at universities in both the UK and US is [Advanced Macroeconomics](https://www.mheducation.com/highered/product/Advanced-Macroeconomics-Romer.html) by [David Romer](https://en.wikipedia.org/wiki/David_Romer) in which it states "incorporating money in models of growth would only obscure the analysis".

Update: since the original time of writing it has become more common to [include money and banking in economic models](https://www.princeton.edu/~markus/research/papers/macro_finance.pdf), though how this took the economics profession until 2008 to make this adjustment seems quite incredible.

### In conclusion

Very low inflation, or deflation is a stress on the economy, increasing the likelihood of companies going bust and therefore raising unemployment. As we have seen in chapter 1, fractional reserve banking is prone to having periods in which the money supply falls and so has a destabilising effect on the economy.

**Did you like contents of this chapter? If not** [**click here**](https://reiss-economics.gitbook.io/book/feedback)**.**